Fiscal policy vs monetary policy

I have researched an advanced idea after having some discussions about the current economic outlooks. In this short 5 minute article, I will try to provide insights in what is currently driving markets and money flows. (Posted Aug 2024).

I have researched an advanced idea after having some discussions about the current economic outlooks. In this short 5 minute article, I will try to provide insights in what is currently driving markets and money flows.

What is the difference with fiscal and monetary policy and have things really changed (post 2020) or are they the same?

Fiscal dominance is a real theme and something I have only started to consider recently. I am just another investor in the market and learn while being exposed to these markets like any other person. We never know everything!

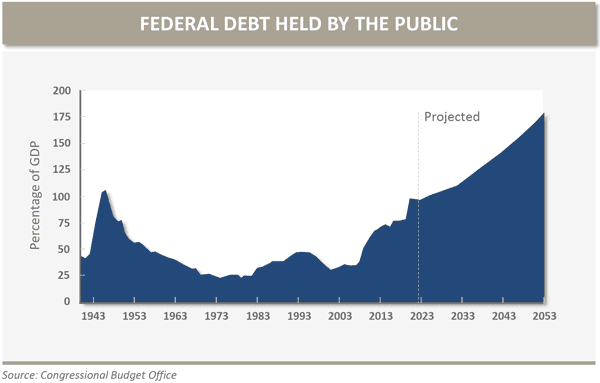

Governments have never been as indebted as they currently are and because of the big deficits at there balance sheets any monetary policy decision (rates) that get set by central banks (FED) may have a 'muted' effect on the control of inflation.

Government deficits currently get refinanced at higher rates (costs go up) and those spendings have to be supported by ** drum sounds ** more printing of money (monetized fiscal spending) rather then by the expansion of bank credit (fractional reserve banking).

This is an inflationary on its own.

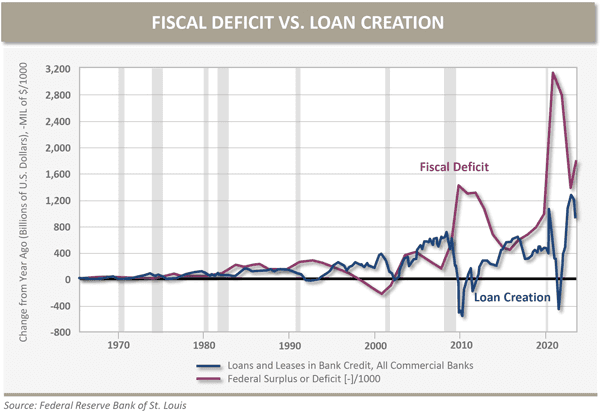

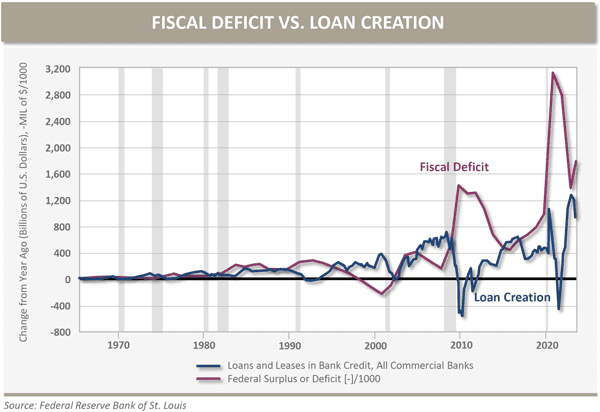

When we take a look at what happened in 2020.

We notice that the fiscal deficit increased much more than the creation of loans. This problem of fiscal dominance is often occuring in countries that are indebted above 100% of their respective GDP. Countries like Argentina and Venezuela come to mind where inflation spirals uncontrollable due to the high amount of money printing.

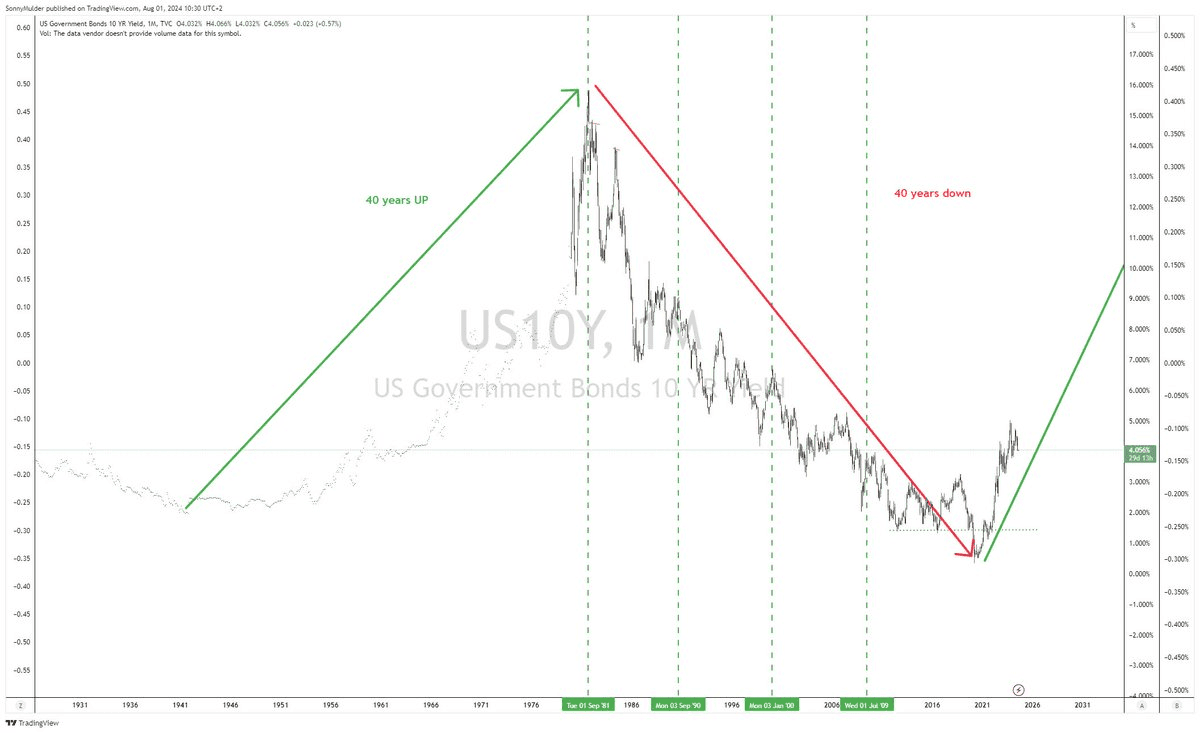

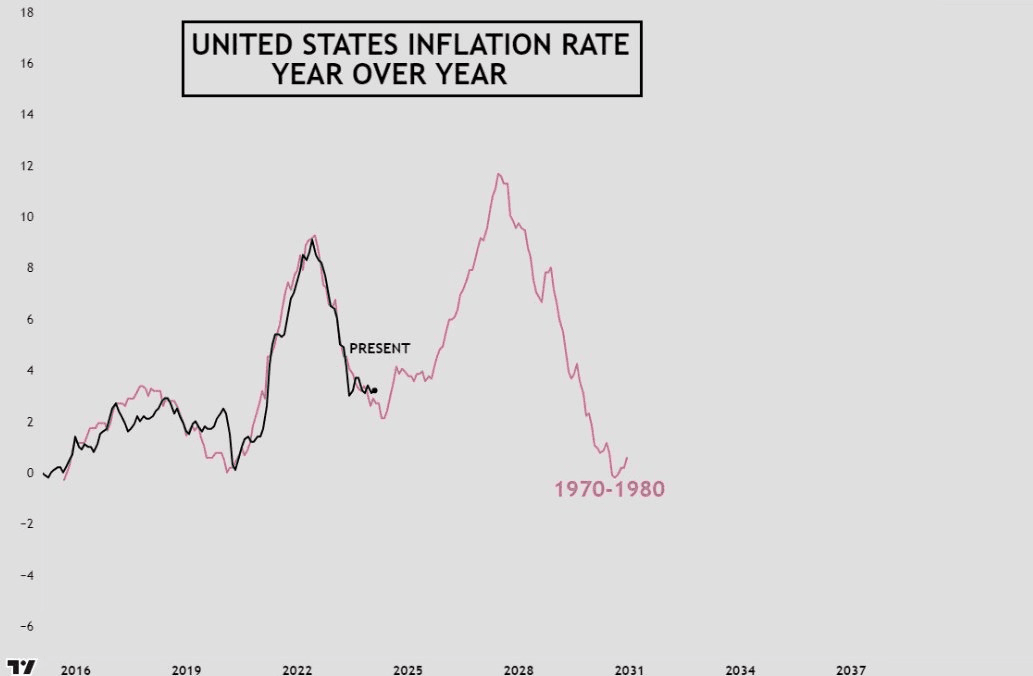

When we compare the yield cycle to historical levels we notice that we likely entered a period where we see higher rates for the next 40 years after making our first higher high.

This could imply inflation could be moving higher after correcting lower medium term, as we have seen in the 80's at the end of that cycle.

This development if it remains an active trend could steer us on the pathway towards policies were yieldcurve control becomes an active measure and where more currency volatility (USD) and inflation are at play.

Asset prices can ramp up hard (post 2020 boom as exmaple) but in real terms could not gain as much to preserve your purchasing power. Real assets will dominate again in this environment. The biggest losers are those who do not hold any kind of assets to preserve or grow their wealth in order to outpace inflation and debasement of currency.

The dynamics of Fiscal dominance, is becoming a more active theme going forward. It could mean there is no 'real terms' recession coming for us in early 2025. Prices stay elevated in various sectors whilst other sectors do go into recession. Think about PMI manufacturing and commercial real estate which are sensitive to higher rates (monetary policy) and look at other services based sectors that have done well so far where earnings are thriving and expansion is still present.

When are we in a fiscal dominant environment?

This occurs whenever we are running high deficits compared to the loan created as is occuring heavily since post 2008 were QE became the norm after grinding at zero rates for years on end.