Oil: The Crude Velocity Trap

What is the effect of oil prices rising on markets and the economy?

A big theme considering the current war with Iran and the USA is the price of oil and its effects on the current economic situation. Let’s take a look at oil and why it is so vital for our economy and how we should interpret price movements.

High oil prices exert significant influence on the economy through interconnected channels that affect inflation, consumer purchasing power and spending, and ultimately GDP growth. These effects stem from oil's role as a critical input in production, transportation, and household budgets. While modern economies are more efficient and less oil-intensive than in the 1970s (oil use per unit of GDP has declined sharply), sustained high prices (above $100–$110) still act as a major drag on consumers and businesses.

How Oil Drives Inflation

Oil price increases contribute to inflation in two main ways:

Direct effects — Crude oil feeds into gasoline, diesel, jet fuel, heating oil, and petrochemicals (plastics, fertilizers, chemicals). Higher crude prices quickly pass through to retail fuel and energy costs, which are components of headline inflation measures like CPI or PCE.

Note: a rough rule of thumb from Federal Reserve analyses is that every $10 increase in crude oil adds about 0.2/0.3% to headline inflation.

Indirect effects — Businesses face higher input costs (transportation, manufacturing, agriculture), which they pass on via higher prices for goods and services. Think: freight costs, airfares, food prices (fertilizer/diesel for farming), and plastics in consumer products. These ripple through supply chains, boosting core inflation modestly but persistently if the shock lasts.

Example: In 2022's Russia-Ukraine spike, oil supply shocks raised core inflation by ~0.17 points annually.

Impact on Consumer Purchasing Power and Spending

High oil prices reduce the real disposable income and purchasing power from households. forcing cutbacks in non-essential spending:

Gasoline and energy bills rise, taking a larger share of budgets (energy is ~3–4% of U.S. household spending, but higher for lower-income groups). This leaves less for retail, dining, travel, entertainment, or big-ticket items like appliances/cars.

Volatile or high prices create uncertainty about future costs, leading consumers to delay purchases. Studies show auto sales dropping sharply in these kind of environments as an example.

Consumers reallocate budgets toward necessities, cutting discretionary categories. This is the typical two tier economic effect we are seeing post 2020 where they are kicking the consumer while they're down, hitting lower/middle-income groups already weakened by rates and softening jobs.

Note: Less spending = lower business revenues = potential layoffs or hiring freezes.

How This Slows GDP Growth

So overall both inflation drags and consumer weakness driven by high oil prices can influence GDP as well:

Lower consumer spending (70% of U.S. GDP is made up of this) directly reduces growth and firms delay expansions.

Resources have to be reallocated from energy intensive sectors, which causes issues in labor and expenses.

Note: $10 oil price increase = ~0.1–0.2 percentage points from annual real GDP growth (Fed estimates; Bank of America 2026 analysis). In severe cases ($120+ or doubling), it risks zero/negative growth or recession.

initial spending drop = slower production = job/income losses = further spending cuts.

Now that we know how oil plays an important role in our economy and US economic data points, let's take a look at the macro picture.

Why is oil still so important in our current economy?

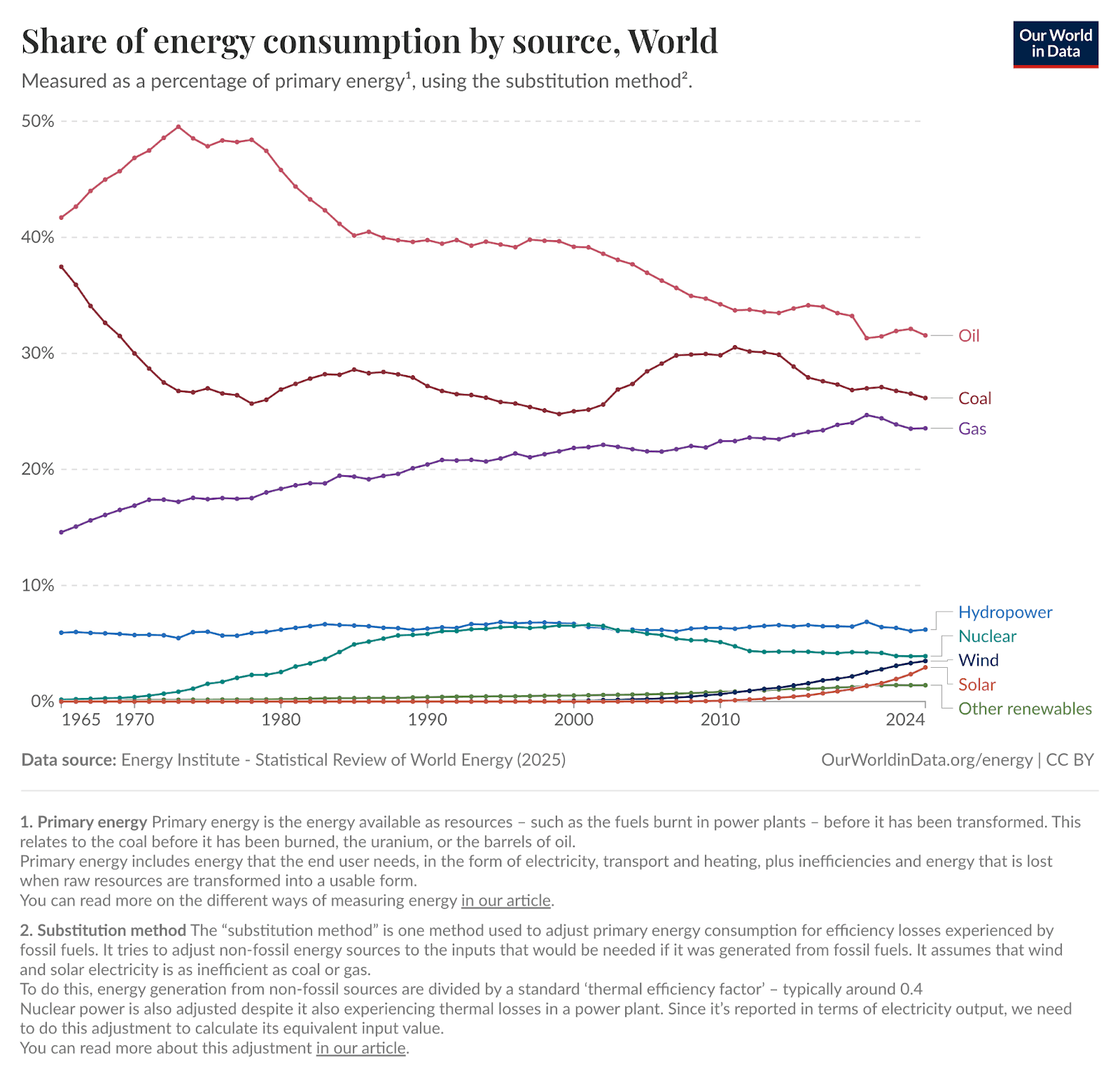

Oil accounts for roughly 30% of global primary energy consumption (its share dipped below 30% for the first time in 2024 after peaking at 46% decades ago). It is irreplaceable in key sectors in the short-to-medium term:

Transportation ~50–60% of demand: gasoline, diesel, jet fuel, and marine fuels have few scalable substitutes at scale right now.

Petrochemicals/feedstocks (plastics, fertilizers, chemicals, synthetic materials) are the fastest-growing segment, up >12% in the past five years (driven by China).

Broader ripple effects: Oil powers trucks that deliver goods, fuels construction/mining equipment, and indirectly affects electricity (in some regions) and heating.

Even with EVs and renewables rising, global demand hit ~103–104 million barrels per day (mb/d) recently, and non-transport uses are structurally hard to decarbonize quickly. The economy’s “oil intensity” has fallen (thanks to efficiency), but absolute dependence remains high, especially in emerging markets!

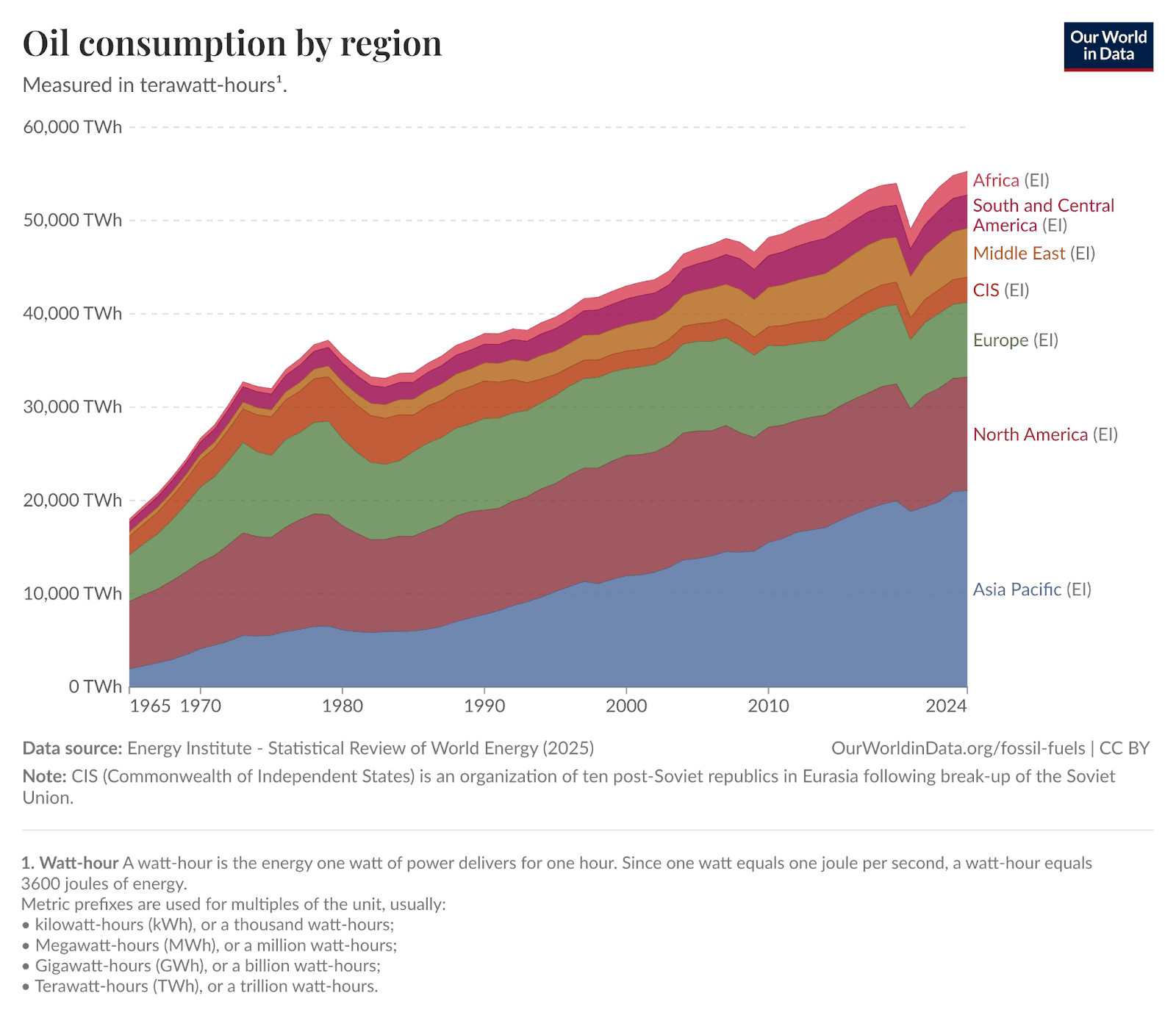

If you look at the data from the Energy institute, then what is very visible is that oil consumption is dropping over the long term. Oil consumption rose sharply after WW2 driven by the rebuild and expansion of the world economies. I believe that in order for our current world to thrive in this new tech heavy revolution (electricity infrastructure build out, datacenters, powergrid build out, …) that we are yet to see demand for oil in the period that lies straight ahead.

Even though oil’s share of total energy has fallen from 46% to ~30%, the actual volume consumed has more than tripled over 60 years because global energy demand overall has exploded.

This is why oil remains irreplaceable in transport, petrochemicals, and industry as barrel usage hits new highs in 2024/25. These two charts together perfectly illustrate the point I made originally: oil’s percentage importance has declined, but its real-world scale and economic centrality have not.

Why high oil prices hurt the economy

As I said at the start of my article, high prices raise input costs across supply chains, trigger inflation and force households/businesses to cut other spending which eventually slows GDP growth. Low price elasticity means people don’t quickly reduce driving or flying but instead, they spend less elsewhere, amplifying slowdowns in the economy.

The FED or other central banks may hike rates to fight inflation caused by price increases (which is one their mandates), further braking growth.

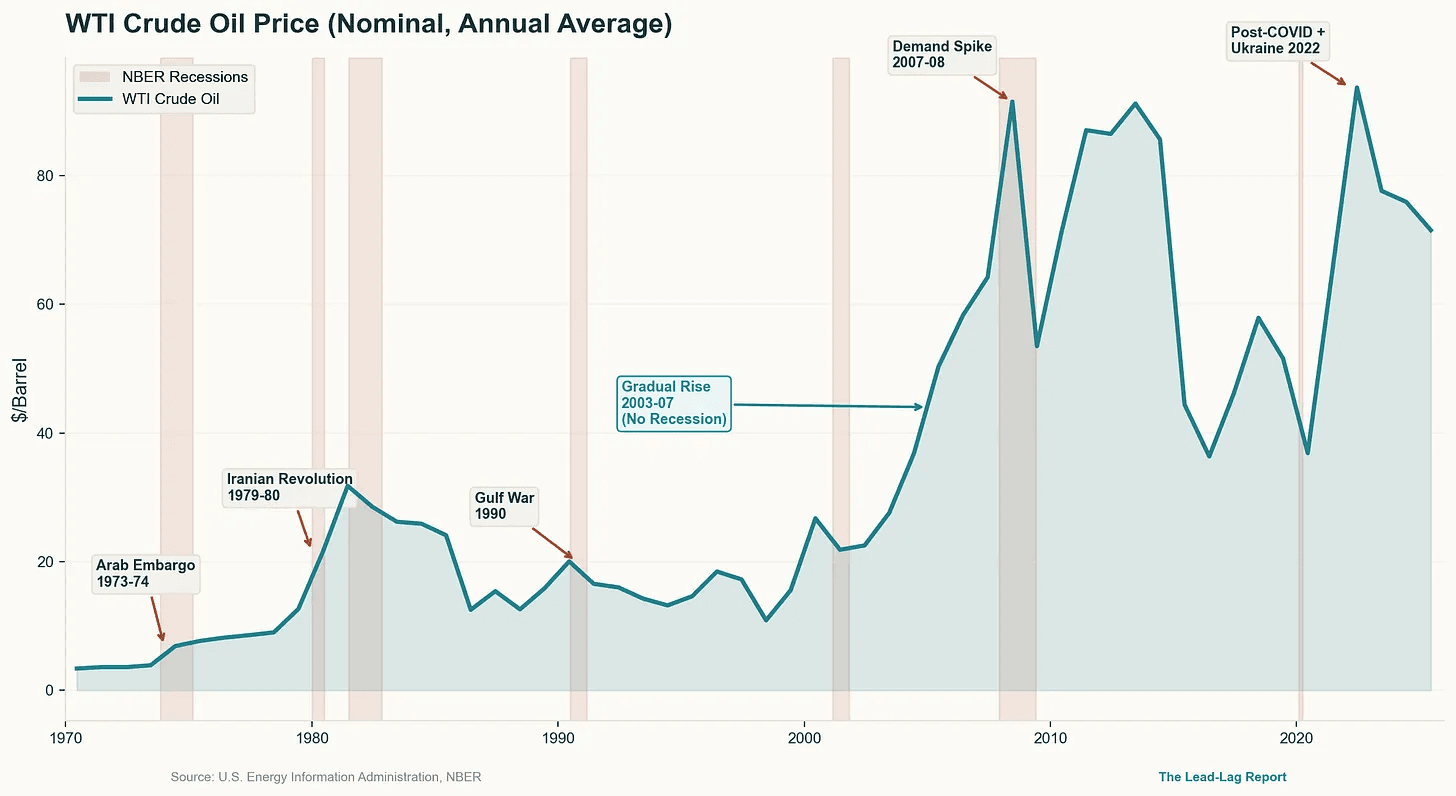

Historic references (every major U.S. recession except one was preceded by an oil price spike):

1973–74 Arab Oil Embargo (Yom Kippur War): Arab OPEC cut production ~7.5% globally; prices quadrupled. U.S. recession (Nov 1973–Mar 1975) with stagflation; GDP fell sharply, gasoline lines formed.

1979 Iranian Revolution + 1980 Iran-Iraq War: Output fell ~7–6% globally; prices more than doubled. Double-dip recessions (1980 and 1981–82); severe inflation and auto sector collapse.

1990 Gulf War: Prices doubled briefly; contributed to 1990–91 recession.

2007–08 spike: Prices peaked near $147 (demand surge + speculation); intensified the Great Recession (mainly financial crisis-driven but oil added drag).

2022 Russia-Ukraine: Prices >$120; fueled global inflation surge and slowdown (though not full recession in all countries).

Below you see clear correlations where high oil price is preceding a recession.

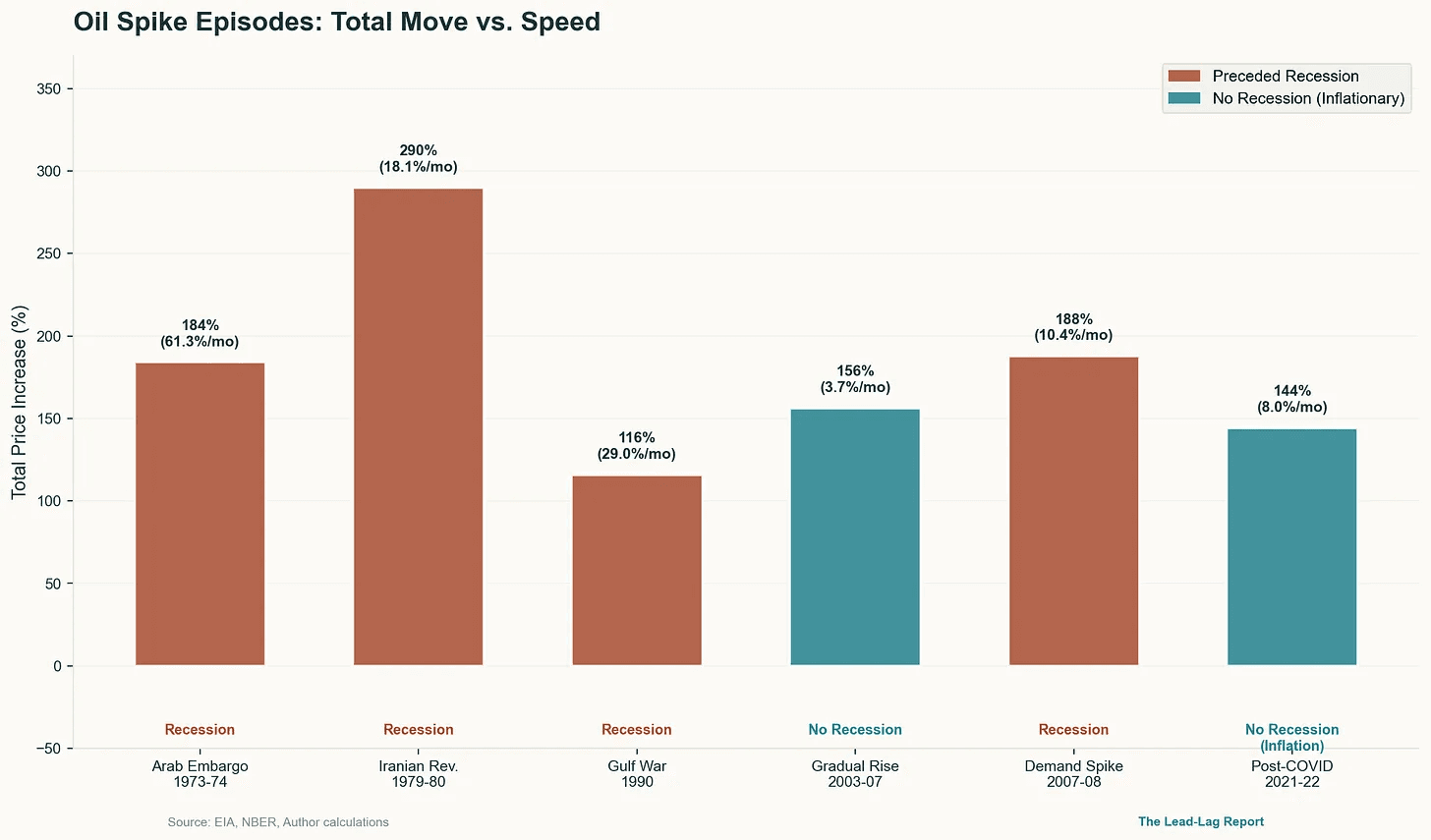

On top of that the actual speed in price increases for oil are also impactful. Even when it does not cause a recession it is likely to cause inflation turning its head back up.

A conclusion from research done by ' ‘The Lead and Lag report’’ clearly states that investors should focus less on whether oil prices will rise and more on how quickly they do. A gradual, demand-driven increase acts as a manageable headwind, fueling modest inflation, pressuring margins, and keeping the Fed watchful,while remaining tradeable and even cycle-extending.

Sharp spikes (especially 50%+ moves in a short window) have historically accelerated the shift from late-cycle strain to outright contraction, acting as a tipping-point accelerant for fragile economies. St. Louis Fed data shows that before the 1973–75, 1980, 1981–82, and 1990–91 recessions, real energy prices surged an average 17.5% in just four quarters, each driven by rapid, concentrated jumps rather than slow grinds.

Macro Geopolitical Implications

Let's take a broad macro look at current oil movements and the geopolitical importance of specific areas and why a war in Iran for instance involving the Strait of Hormuz could be a case for a supply disruption worldwide that has major ramifications on the macro economy as a whole.

Total oil production meets 108 mb/d total liquids. The top producers are the USA (13,6mb/d), Saudi Arabia, Russia, China, Canada, Iraq, UAE and some other non-OPEC countries like Brazil.

The United States and China are the largest consumers. China is the #1 importer (growing petrochemical demand); India, Europe, Japan/South Korea are also heavy importers. Roughly 70–80% of seaborne oil trade passes through narrow maritime chokepoints and disruptions here cause instant global price spikes because alternatives are limited/slower. Below I will provide the most important crosspoints for ships and any disruption to these can cause major disruption worldwide:

Strait of Malacca (between Malaysia and Indonesia): ~23.2 mb/d

→ ~22% of global oil consumption; ~29% of total maritime oil trade.

(World's busiest chokepoint by volume; key route for Middle East oil to Asia.)

Strait of Hormuz (between Iran and Oman): ~20.9 mb/d

→ ~20% of global oil consumption; ~25–26% of maritime oil trade.

(Carries nearly all Persian Gulf exports from Saudi Arabia, Iraq, UAE, Kuwait, and Iran; 80–90% to Asia, especially China, India, Japan, South Korea.)

Cape of Good Hope (around southern Africa): ~9.1 mb/d

→ ~9% of global oil consumption; ~11% of maritime oil trade.

(Alternative routes when Suez/Bab el-Mandeb are disrupted; volumes have risen due to recent Red Sea issues.)

Suez Canal (Egypt, often combined with SUMED pipeline): ~4.9 mb/d

→ ~5% of global oil consumption; ~6% of maritime oil trade.

(Links Mediterranean to Red Sea; volumes halved from 2023 peaks due to regional disruptions.)

Bab el-Mandeb Strait (between Yemen and Djibouti/Eritrea): ~4.2 mb/d

→ ~4% of global oil consumption; part of the Red Sea corridor to Suez.

(Connects Gulf of Aden to Red Sea; frequently disrupted, leading to rerouting around Cape of Good Hope.)

Oil price expectations for the next years.

We now know what oil can do to our economy and what bottlenecks we need to watch. We know that short or long term price spikes have different effects but what is my personal outlook for oil in the years that lie ahead? Let’s give you both a bull and bearish case.

In the very short term I see that markets are currently oversupplied (inventories building ~2–3 mb/d in recent forecasts), but geopolitics (Middle East/Hormuz disruptions) have caused spikes. Energy Information Administration’s latest Short-Term Energy Outlook (March 2026) projects Brent averaging ~$79/b in 2026 and ~$64/b in 2027, with global supply outpacing demand and U.S. production rising to 13.8 mb/d.

Next +/- 8 years:

Bearish narrative: Demand growth slows sharply driven by EVs, increased efficiency from industrials and renewables. A possible plateau or peak before or around 2030 under current policies with declines after that period. Those declines align with long term cyclicals for US equities (a cycle peak around 2030 followed by bear market) could suppress oil prices in the future. Oversupply from non-OPEC in combination with a weak macro environment overall equals downward price pressure while the energy transition continues to accelerate. So basically oil needed for economic expansion goes down even in Emerging markets.

Bullish narrative: Demand keeps growing (petrochemicals + emerging markets offset transport losses). Economic expansion driven by tech adoption, think datacenters, infrastructure upgrades, cause an increased need for oil worldwide. Underinvestment in upstream infrastructure and refining (Green Deal push worldwide) creates future supply crunches. Geopolitics and OPEC+ discipline supports higher prices because demand stays but supply continues to weaken as infrastructure stays behind. I have talked about this in another article I wrote ‘’The new MOAT in town: Energy’’ where I speak about the AI push and the implications for the energy grid and sector as a whole.

My main take in this article is that infrastructure expansion is limited and new oilfields and refinery buildout is a bullish factor, if demand holds longer than expected, shortages could emerge in the early 2030s, pushing prices up. However oil is very sensitive to geopolitics and the decrease in its overall share as primary energy does not work in our favor for the bulls. I am looking mostly at investors positioning themselves in the sector (Energy) because they anticipate tech and infrastructure build out. It may not be factual in the end but we all know that investors are looking for the next big narrative and they look far ahead when they position for investments.

I remain structurally bullish on the energy sector and believe it will be a profitable theme in the years ahead. Not only because of Energy itself but also because of structural issues in Europe and other countries. I believe that opportunities lie in infrastructure and services as part of a well diversified portfolio.